Pick Up

1513. Global Food Price Trends – May 2026

Related Research Program

Information

1513. Global Food Price Trends – May 2026

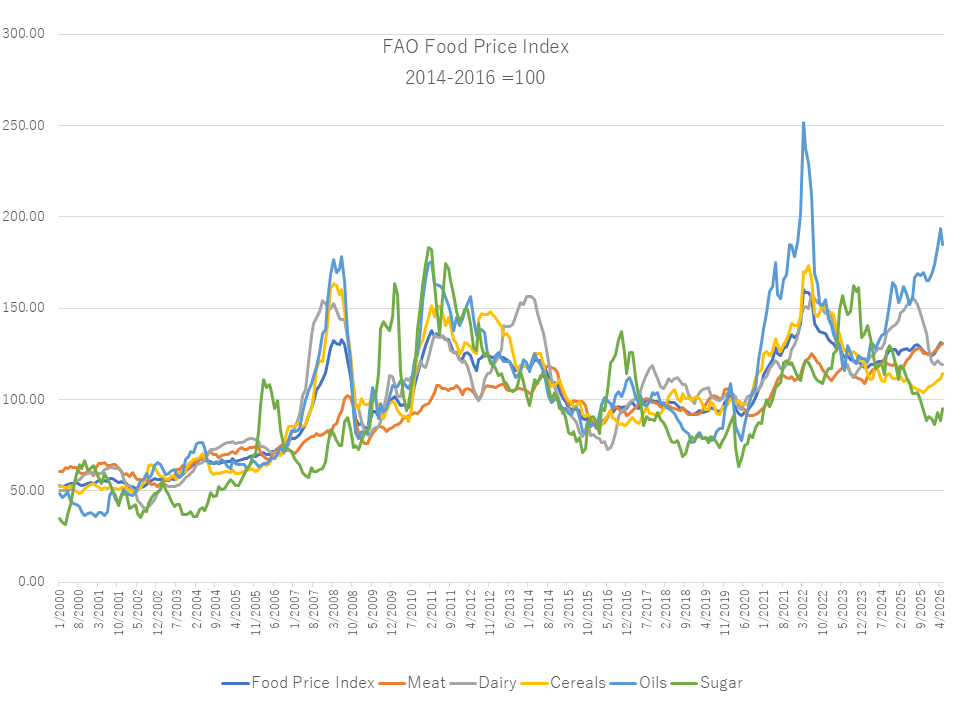

The FAO Food Price Index (FFPI) averaged 130.8 points in May 2026, remaining broadly stable compared with April (down 0.2 percent month-on-month). Increases in the cereal and sugar price indices were offset by declines in vegetable oil and dairy prices, while the meat price index remained nearly unchanged. Compared with historical levels, the FFPI stood 2.9 percent above its value a year earlier but remained 18.4 percent below its all-time high recorded in March 2022.

The FAO Cereal Price Index averaged 114.3 points in May, up 2.6 percent from April and 4.9 percent higher than a year earlier. Wheat prices rose for the fourth consecutive month, supported by poor winter wheat conditions in the United States and worsening harvest prospects among major exporters. Higher fuel and fertilizer costs also added upward pressure. Maize prices increased due to stronger import demand from key markets, concerns over tightening supplies in Brazil and the United States, and robust ethanol demand linked to higher energy prices. Sorghum and barley prices also rose, reflecting tighter global maize and wheat markets. The FAO All Rice Price Index increased by 2.7 percent, supported by weather-related concerns and higher crude oil prices in major Asian exporting countries.

The FAO Vegetable Oil Price Index averaged 185.0 points in May, down 4.6 percent from April, marking its first monthly decline since the beginning of 2026. International palm oil prices fell amid expectations of weaker global import demand and uncertainty in crude oil markets. Soybean oil prices faced downward pressure from increasing exportable supplies in South America, although strong biofuel demand in the United States provided support. By contrast, rapeseed and sunflower oil prices increased, reflecting tighter supplies in the European Union and Ukraine.

The FAO Meat Price Index was virtually unchanged from April, increasing by only 0.1 percent, but remained 6.3 percent above its level a year earlier. Beef prices continued to rise, driven by strong import demand, particularly from China and the United States, together with supply constraints associated with herd rebuilding in major producing countries. Sheep meat prices also increased due to limited supplies in New Zealand. In contrast, pig meat prices declined, reflecting abundant supplies and subdued import demand in the European Union. Poultry meat prices recorded a modest increase, supported by firm demand for Brazilian exports.

The FAO Dairy Price Index declined by 0.5 percent from April and was 22.4 percent lower than a year earlier. Butter prices continued to fall in Europe and Oceania as improved milkfat availability and intensified export competition weighed on the market. Cheese prices also declined slightly. In contrast, skim milk powder prices increased, supported by firm import demand from the Near East, North Africa, and parts of Asia. Whole milk powder prices remained broadly stable, as stronger prices in Oceania due to tightening export availability were largely offset by weaker quotations in Europe amid subdued demand from China.

The FAO Sugar Price Index rose by 7.5 percent from April, reaching its highest level since October 2025, although it remained 13.1 percent below its level a year earlier. The increase was mainly driven by concerns over tighter global sugar supplies in the coming months. In Brazil, expectations that a larger share of sugarcane would be diverted to ethanol production raised concerns about reduced sugar output. Additional support came from concerns that anticipated El Niño conditions later in 2026 could adversely affect sugar production in India and Thailand, potentially reducing global export availability.

Overall, global food prices remained relatively stable in May 2026. However, upward pressure on cereal prices and growing concerns over sugar supplies suggest increasing market uncertainty. In particular, deteriorating weather conditions in key producing regions and the potential development of El Niño are likely to remain important risk factors for global food markets in the months ahead.

Contributor: IIYAMA Miyuki, Strategic Coordination Office