Pick Up

1459. How War with Iran Threatens Global Food Security

Related Research Program

Information

1459. Chokepoint: How War with Iran Threatens Global Food Security

The term "chokepoint" is used not necessarily to refer to a physical "narrowness," but rather to a critical point that restricts flow or movement.

Transportation, Logistics, and Geographic Context

- "Bottleneck": A point where traffic volume is concentrated, causing congestion or stagnation.

- "Narrow Road" or "Transportation Hub": A geographical location where through traffic is restricted.

Business, Economics, and Network Context

- "Bottleneck": A factor that limits processing capacity or supply.

- "Point of Dominance" or "Control Point": A crucial point with significant influence.

Military and Strategic Context "Strategic Point" or "Key Location": A location that is likely to hinder enemy advances or transportation.

The Center for Strategic and International Studies (CSIS), a US think tank, has discussed the impact of the Strait of Hormuz choke point, resulting from the war with Iran, on global food security.

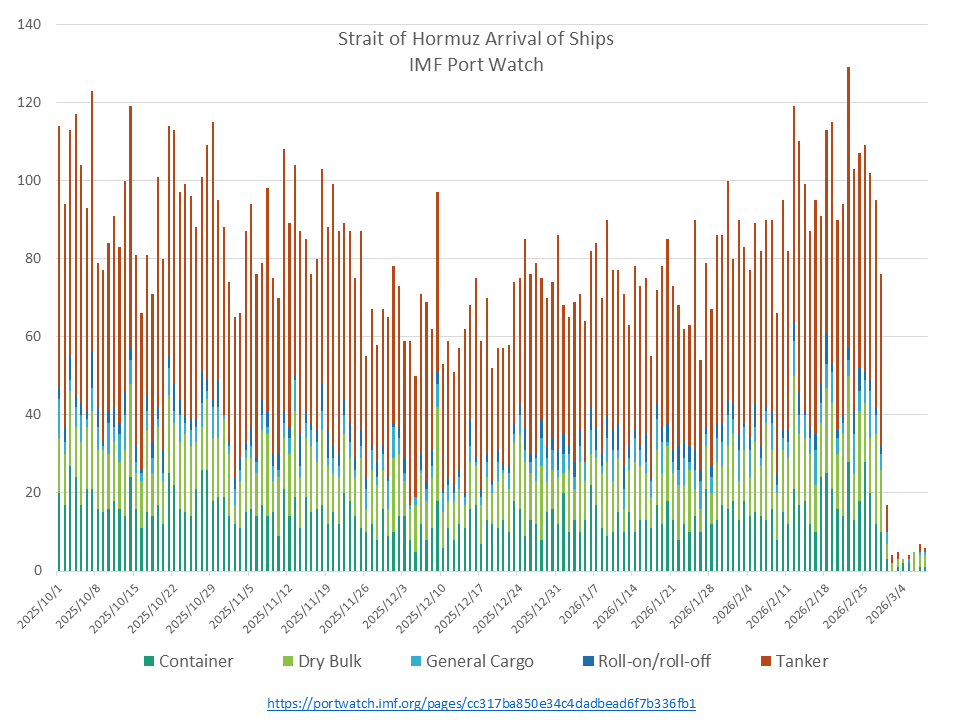

Following the joint US-Israeli attack on Iran on February 28, and subsequent Iranian attacks across the Middle East, the Strait of Hormuz has been effectively closed, putting pressure on a critical choke point in the global oil, natural gas, and fertilizer trade. Fertilizer prices are soaring, and farmers in the Northern Hemisphere are deeply concerned about short-term supply instability ahead of the spring planting season. How will this conflict affect global fertilizer and agricultural markets, and which countries will be most affected? Will current shocks in the energy and fertilizer markets lead to a long-term food security crisis?

Q1: How will this conflict affect global fertilizer markets?

A1: Of the three main nutrients used in fertilizers—nitrogen, phosphorus, and potassium—nitrogen is the most consumed, accounting for approximately 59% of total global fertilizer use in 2023, followed by phosphorus at 21% and potassium at 20%. Nitrogen is essential at every stage of the growth cycle, including protein synthesis and photosynthetic efficiency (and consequently crop yield). Approximately 45% of global nitrogen fertilizer use is for cultivating major grain crops such as wheat, rice, and corn, which supply more than 40% of the world's calorie intake. The Middle East is a major exporter of liquefied natural gas (LNG), a key raw material for synthetic nitrogen fertilizers, and of fertilizers themselves, including the most common nitrogen fertilizers, urea and ammonia. The Strait of Hormuz supports 20% of global LNG exports and 20-30% of global fertilizer exports (35% of urea exports). Approximately 20% of the global phosphate fertilizer trade is supplied by countries affected by the turmoil in the Strait of Hormuz or the broader regional conflicts. Furthermore, sulfur, a byproduct of oil and gas refining, is essential for phosphate fertilizer production, and approximately 45% of the global sulfur trade is affected by the disruption caused by this conflict. At the same time, other major fertilizer suppliers have been unable to increase production to compensate for the decrease in supply from the Middle East. Russia accounts for about one-fifth of the global fertilizer trade and 14% of global nitrogen fertilizer exports, but is facing domestic export restrictions and attacks on production plants by Ukraine, and companies are reportedly focusing on meeting domestic demand. China imposed export restrictions on phosphate fertilizers in the spring of 2021 to ensure stability in fertilizer prices in its domestic market. These restrictions expire in August of this year, but given the recent market turmoil, China may extend them to protect its domestic market.

Q2: How are global fertilizer and food markets reacting to this conflict?

A2: The blockade of the strait is seen as a "worst-case scenario" for the global fertilizer market. Fertilizer prices rose immediately after the conflict began, and by March 11, global urea prices had risen by approximately 26%, from $465.50 per ton to $585 compared to pre-war prices. If the disruption continues, the effects could ripple globally in the form of increased input costs, reduced yields, and ultimately, soaring food prices. Asian markets are particularly vulnerable. In 2024, 83% of liquefied natural gas (LNG) passing through the Strait of Hormuz was destined for the Asian market. India, in particular, is facing imminent pressure from fertilizer manufacturers to reduce urea production due to rising production costs caused by soaring LNG prices, ahead of the monsoon season starting in June and the peak fertilizer demand a few months later. This pressure is spreading across the region, with granular urea prices in Southeast Asia soaring by more than 40% since the conflict began. While Brazilian authorities, the world's largest importer of fertilizer, say they are well-prepared to handle short-term disruptions, long-term disruptions to production and transportation in the Middle East, a major supply region, could lead to increased costs for Brazilian farmers. Sub-Saharan Africa already uses relatively little fertilizer, but many African producers lack the financial resources to absorb the price increases and may reduce their use, raising concerns about worsening food insecurity for farmers who depend on local markets. The impact on agricultural prices is still unclear, but rising fossil fuel prices make renewable fuels derived from agricultural products such as soybeans and corn more attractive, and soybean oil futures prices hit a two-and-a-half-year high in the first week after the war began. For similar reasons, Brazilian sugar mills are expected to prioritize the production of sugarcane-derived ethanol, which could lead to higher global sugar prices.

Q3: How vulnerable is US agriculture to disruptions in the fertilizer market?

A3: The US is heavily reliant on imports of nitrogen fertilizers, with Russia and Qatar being the main suppliers of urea. The closure of the strait is particularly ill-timed for US farmers, as the US fertilizer market lacks strategic reserves, and a rapid expansion of domestic production to compensate for a sudden import disruption is considered impossible, especially during the spring planting season. Corn, which uses a large amount of nitrogen fertilizer, is the most vulnerable, and a sharp rise in fertilizer prices would rapidly improve the relative profitability of soybeans, a trend already impacting planting area forecasts.

Global impacts are already being seen, and without diplomatic assurances, the risk of long-term consequences will accelerate. Several factors will influence the severity of the downstream impacts, including whether China reconsiders export restrictions beyond the closure of the Strait of Hormuz, how many fertilizer factories suspend or adjust operations, the concrete impact of the sharp drop in fertilizer prices on planted area and productivity, and how agricultural futures prices move as the spring planting season begins.

Contributor: IIYAMA Miyuki, Information Program